| Even though Wisconsin’s Constitution calls “…for the establishment of district schools which shall be as nearly uniform as practicable…,” the Association for Equity in Funding believes there are three main reasons why the schools are not uniform. They are unequal property wealth, unequal concentration of students with additional educational needs and state payments which do not equalize wealth or address the cost of meeting additional educational needs.

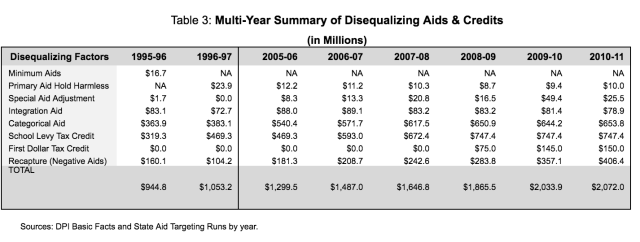

Disequalizing factors in our school finance system continue to increase, and it is difficult to understand how children can receive an equal opportunity for a sound basic education when districts are becoming less uniform. Those disequalizing factors need to be revised or eliminated in order to make schools more uniform and enable all districts to provide an equal educational opportunity. Variation in Local Property Wealth Throughout the state there is a wide variation in the amount of public funds invested to educate our children. And there is a wider variation in the property tax rates paid by property owners to support public schools. K-12 spending per pupil (Comprehensive Costs from Annual Reports per DPI Basic Facts) for 2008-09 ranged from $10,293 in Elk Mound to $23,679 in Phelps (a high/low ratio of 2.3 to 1) with a state average of $12,346. K-8 spending ranged from $10,292 in Randall J1 to $22,518 in Lac du Flambeau #1 (a high/low ratio of 2.2 to 1). K-12 property tax rates in 2009 (per WTA SchoolFacts10) ranged from $2.71/M in Gibraltar to $15.35/M in Elmwood (a high/low ratio of 5.7 to 1) and the state average was $9.18. The district with the lowest property tax rate (Gibraltar budgeted $17,897) spent more money per pupil than the district with the highest property tax rate (Elmwood budgeted $15,388). These disparities highlight a growing concern about the lack of fairness in the funding of elementary and secondary education in Wisconsin. Because the system still depends on local property wealth as a major source of funding, the wide variation in the property tax levels cannot be ignored. Its cumulative impact will be played out in classrooms and in the lives of students as they grow up. Disequalizing Payments Other school aid and credit programs that do not consider relative property wealth have contributed to the problem. All districts (or their taxpayers) receive extra money for specific programs (such as special adjustment aid, school levy tax credits, categorical aid and integration aid), regardless of wealth or tax effort. This off formula funding tends to distort the equalizing aspects of the school aid formula and give more money to property wealthy districts and their taxpayers. Table 3, below, shows generally increasing overall state expenditure for disequalizing factors in school funding (See Glossary for additional explanation). The school levy credit was increased by $123.7 million for 2006-07, by $79.3 million in 2007-08, and by $75 million in 2008-09. The First Dollar Tax Credit was added in 2008-09 and totals $150 million in 2010-11. Distribution of funds in these programs ignores the variation in the tax base behind each pupil. All disequalizing factors should be eliminated, and aid payments to school districts should be equalized.

Disabilities, Poverty and English Learners Our Supreme Court has directed that districts with disproportionate numbers of children with disabilities, children who are economically disadvantaged, and children with limited English language skills be taken into account. The additional educational needs of each of these populations can best be addressed through an equalized pupil weighting which would increase the pupil count for both aid and revenue limit purposes. Although the Student Achievement Guarantee in Education (SAGE) program is well accepted and attempts to meet some of these student needs, it has not reached some high poverty schools. The per-pupil grant has never been increased, and it provides no benefit for children in grades 4-12. Consequently, some of our economically disadvantaged children who need additional help are not receiving it. The proportion of costs covered by the categorical aid appropriations for disabled children and children with limited English language skills continues to decline. Due to the projected state budget deficit these separate appropriations in our current system are likely to be ignored and/or underfunded in the foreseeable future even though our standard requires that these student populations be taken into account. Related matters During the 1990’s we saw a good economy which increased residential property values, produced rising incomes for many and maintained low interest rates. Accordingly, it became easier for some to purchase and improve real estate. One of the results was a greater demand for lake and recreational property, and this increased the equalized valuation in many school districts. When combined with enrollment declines in some districts, these higher values have led to lower levels of state support and higher local school property taxes. As a result, some have called for the inclusion of an income factor in the school equalization aid formula. But there is a better answer to this problem, and it is the Homestead Tax Credit program, which helps low income households pay their property taxes. First, consider there already is some recognition of income and ability to pay in the school finance equation as the state share of school costs comes mainly from state income and sales taxes. Second, consider that public schools essentially have only one source of revenue other than state aid and it is the property tax. Third, our educational standard requires that economically disadvantaged students be taken into account in the school finance system. So, what is fair? The state income tax treats us all in the same manner and imposes a lesser burden on low income households. AEF has tried to equalize access to state and local resources through the equalization aid formula so that the school property tax burden would be spread fairly. The Wisconsin Supreme Court has recognized that economically disadvantaged students are likely to need additional help in or order to succeed in school. Ideally, the legislature would revise the school finance system to provide equal access to state and local revenues and provide inflation-sensitive assistance to all economically disadvantaged students. Then the Homestead Tax Credit program, set at an appropriate level, would help to fairly ease the tax burden on low income households. As this is a state taxation issue and not a school finance issue, AEF offers no specific proposal on the Homestead Tax Credit program at this time. Rather, AEF will continue to focus on the financing of public schools under our educational standard. |